How to Calculate 401k Contribution on Paycheck 2026 Guide

To calculate your 401k contribution, multiply your Gross Pay (total earnings before taxes) by your Contribution Percentage. For example, if your bi-weekly gross pay is $2,500 and you contribute 6%, your deduction is $150. This amount is typically taken out “pre-tax,” meaning it lowers your taxable income and reduces the amount of federal income tax you owe today.

The 401k Deduction Formula

To visualize how this works on your paycheck, use this simple mathematical framework:

Gross Pay per Pay Period × Contribution Percentage = Your 401k Deduction

Example: $3,000 (Gross Pay) × 0.05 (5% Contribution) = $150

2026 401k Limits: Fast Facts

Knowing the math is only half the battle; you also need to know the IRS “speed limits” for 2026 to ensure you don’t over-contribute.

Individual Employee Limit: $23,500 (Approximately $1,958 per month)

Catch-up Contribution (Age 50–59): $7,500 (Adds about $625 per month)

Super Catch-up Contribution (Age 60–63): $11,250 (Adds about $937 per month)

Total Limit (Employee + Employer Combined): $70,000 (Approximately $5,833 per month)

Why This Matters for Your Take-Home Pay

In 2026, every dollar you contribute to a Traditional 401k reduces your taxable income dollar-for-dollar. This means a $100 contribution won’t actually “feel” like $100 is missing from your wallet. Because of tax savings, your net take-home pay might only drop by $75 to $85, depending on your tax bracket. It is one of the most efficient ways to pay your “future self” while saving on taxes today.

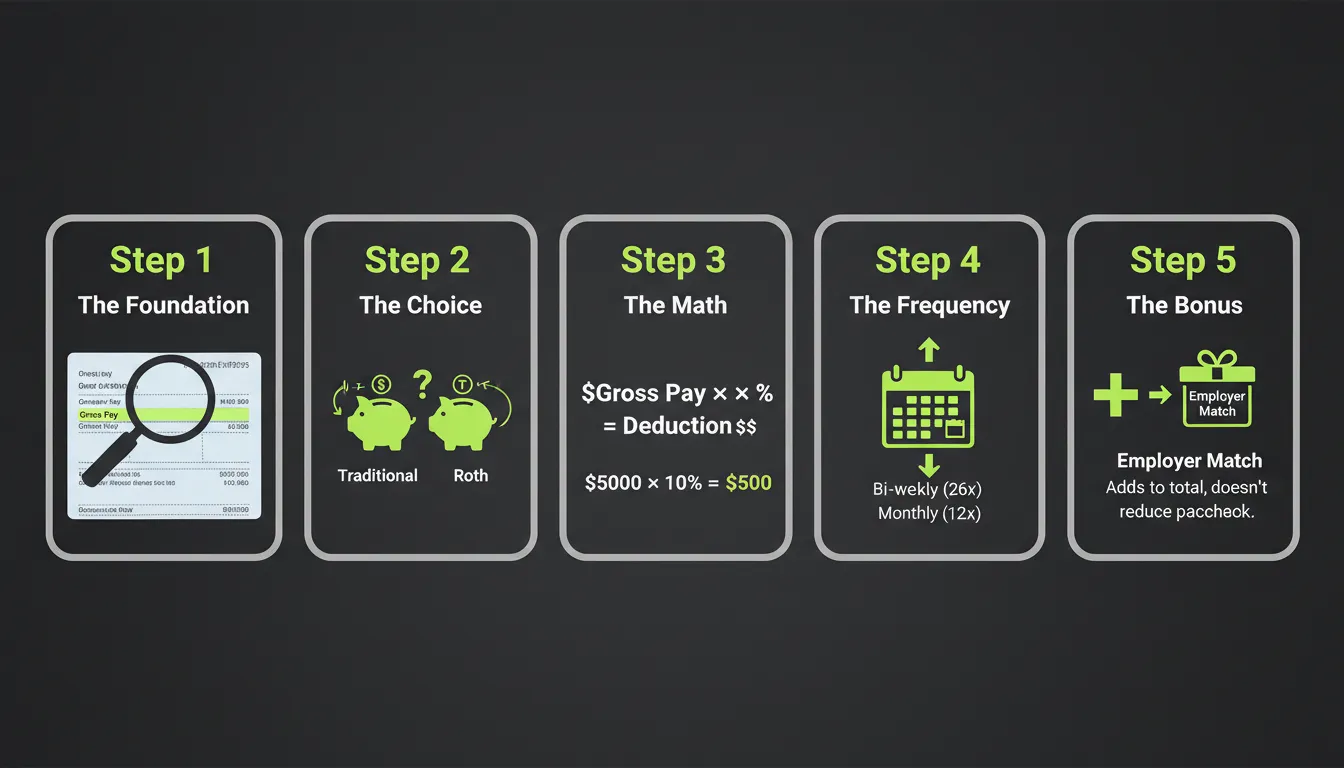

5 Steps to Calculate Your 401k Deduction Manually

Calculating your retirement savings shouldn’t feel like a complex math exam. Unlike other calculators that overwhelm you with forms, we have broken it down into five simple, logical steps.

Step 1: Find Your Gross Pay

Your gross pay is the total amount you earn before any taxes, health insurance, or other deductions are taken out. You can find this at the top of your most recent pay stub. If you are salaried, divide your annual salary by the number of pay periods in a year.

Step 2: Choose Your Contribution Type

You must decide how you want your money taxed. This is a critical step because it changes the “timing” of your tax savings:

Traditional 401k (Pre-tax): Money is taken out before federal income taxes are applied. This lowers your tax bill today.

Roth 401k (After-tax): Money is taken out after taxes are paid. You don’t save on taxes now, but your withdrawals in retirement are tax-free.

Step 3: Apply Your Contribution Percentage

Now, take your gross pay from Step 1 and multiply it by the percentage you have chosen to contribute.

The Math: Gross Pay × (Contribution Percentage / 100)

Example: If your gross pay is $2,500 and you choose to contribute 6%, the calculation is: $2,500 × 0.06 = $150.

Step 4: Consider Your Pay Frequency

Your paycheck impact depends on how often you get paid. To find your annual contribution, multiply your per-paycheck deduction by your annual pay frequency:

Weekly: 52 paychecks per year.

Bi-weekly: 26 paychecks per year.

Semi-monthly: 24 paychecks per year.

Monthly: 12 paychecks per year.

Step 5: Factor in the Employer Match The "Free Money"

Most employers will match a portion of your contribution (e.g., 50% of the first 6%). This is added to your account but does not come out of your paycheck.

Example: If you contribute $150 and your employer matches 50%, they will add an extra $75 to your account.

Total Savings: Your $150 + Employer’s $75 = $225 total monthly savings.

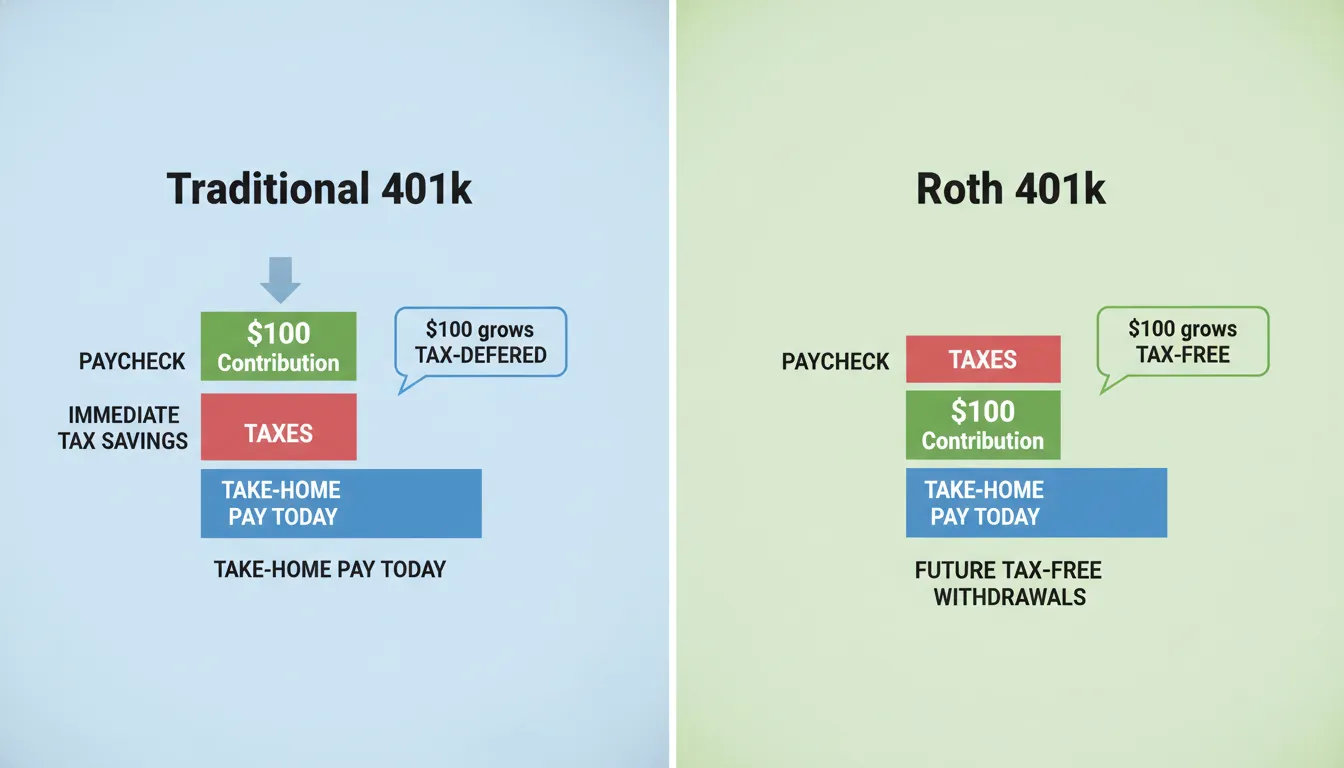

Traditional 401k vs. Roth 401k: Which One Impacts Your Paycheck More?

One of the biggest points of confusion for employees is choosing between a Traditional and a Roth 401k. While both help you save for retirement, they affect your current take-home pay in very different ways. Understanding this “Value Gap” is the secret to maximising your savings without feeling a massive squeeze on your monthly budget.

The "Take-Home Pay" Secret

The most important thing to know is that a Traditional 401k costs you less today.

Because Traditional contributions are taken out pre-tax, they lower your total taxable income. For example, if you earn $3,000 and put $200 into a Traditional 401k, the IRS only taxes you as if you earned $2,800. This “tax shield” means your actual take-home pay only drops by about $150 or $160, even though you saved a full $200!

In contrast, a Roth 401k is funded with after-tax dollars. You pay your full tax bill first, and then the contribution is deducted. While this means you pay no taxes when you withdraw the money in retirement, it results in a larger immediate “hit” to your current paycheck.

Comparison: Traditional vs. Roth Impact

To keep it simple, here is how the two compare across the most important categories:

Tax Timing:

Traditional: You save on taxes Now (Pre-tax).

Roth: You save on taxes Later in retirement (Post-tax).

Taxable Income:

Traditional: Lowers your taxable income today.

Roth: Has no effect on your taxable income today.

Paycheck Impact:

Traditional: Lower Impact. Your take-home pay stays higher.

Roth: Higher Impact. You see a larger reduction in your take-home pay.

Best For:

Traditional: People in high tax brackets who want to save money on taxes right now.

Roth: People who expect to be in a higher tax bracket when they retire.

401k Impact on Different Salary Levels

To give you a clear picture of how these numbers translate to real life, let’s look at two common scenarios. These examples demonstrate how 401k contributions interact with tax brackets and take-home pay in 2026.

Case 1: The $50,000 Annual Salary (5% Contribution)

In this scenario, we have an individual earning a moderate income who wants to start consistent savings.

Gross Pay (Bi-weekly): ~$1,923

401k Contribution (5%): $96.15

The Reality Check: Because this is a pre-tax contribution (Traditional 401k), the employee doesn’t actually “lose” $96.15 from their paycheck. Since their taxable income is lowered, they save roughly $12–$20 in federal taxes per check.

Actual Paycheck Impact: Their take-home pay only drops by approximately $76–$84, yet they have $96.15 growing in their retirement account.

Case 2: The $100,000 Annual Salary (Max-Out Strategy)

For high earners, the goal is often to hit the IRS limit ($23,500 for 2026) to maximize tax tax savings.

Gross Pay (Bi-weekly): ~$3,846

401k Contribution (to Max Out): ~$904 per paycheck

The Tax Shield: At this income level, the employee is likely in a higher tax bracket (22% or 24%). By contributing $904 pre-tax, they significantly reduce their taxable income.

Actual Paycheck Impact: While $904 goes into their 401k, their take-home pay might only decrease by around $680–$700. They are essentially getting a massive “discount” on their retirement savings thanks to immediate tax relief.

The Bonus Paycheck: How Deductions Work on Extra Income

This is a major “content gap” that many competitors miss. Users often ask: “Will my 401k be taken out of my annual bonus?”

The Answer: In most cases, yes. Most payroll systems apply your standard 401k percentage to all supplemental wages, including bonuses. If you receive a $5,000 performance bonus and your contribution rate is 10%, $500 will be diverted to your 401k.

Pro-Tip: If you are close to hitting the annual IRS limit ($23,500), a large bonus deduction could cause you to “Max Out” earlier in the year than expected. Always check if your employer offers a “True-up” contribution to ensure you don’t miss out on employer matching if you stop contributing mid-year.

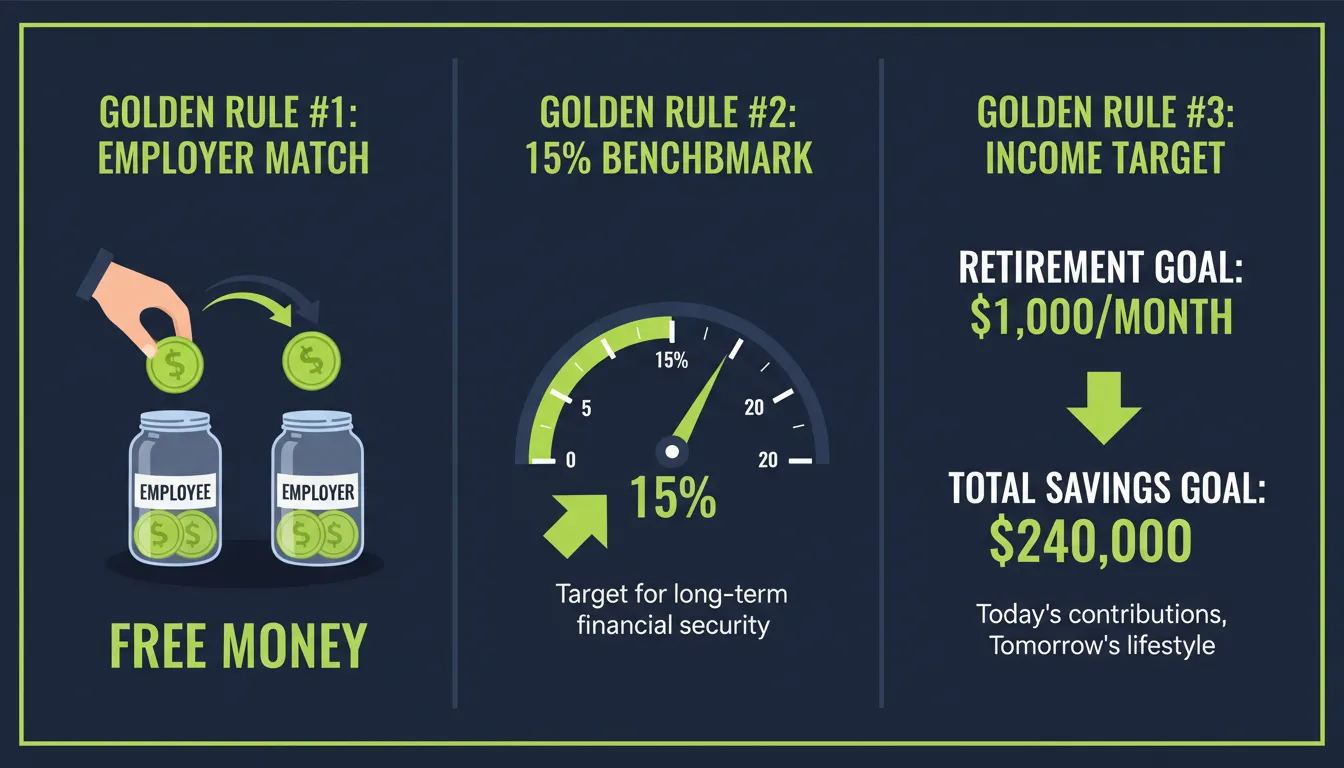

How Much Should You Contribute? (The "Golden" Rules)

Figuring out the “perfect” percentage to deduct from your paycheck can be overwhelming. While everyone’s financial situation is unique, there are three industry-standard “Golden Rules” that can help you decide.

The 15% Rule: The Industry Benchmark

Most financial experts suggest aiming for a total contribution of 15% of your gross income.

Is 7% a good amount? It’s a great start! If you are in your 20s, 7% combined with a long time horizon can grow significantly. However, as you progress in your career, experts recommend inching that number closer to 15%.

The 1% Strategy: If 15% feels impossible right now, start where you are comfortable and increase your contribution by just 1% every year or whenever you get a raise. You’ll hardly notice the difference in your paycheck, but your future self will thank you.

The "Employer Match" Rule: Don’t Leave Money on the Table

This is the most important rule in retirement planning. If your employer offers a match (e.g., “we match 50% of what you put in, up to 6% of your salary”), your absolute minimum goal should be to contribute enough to get that full match.

Why? An employer match is essentially a 100% or 50% guaranteed return on your money instantly. No other investment in the world offers “free money” with zero risk like this.

Example: If you earn $60,000 and your employer matches up to 6%, contributing at least $3,600 a year ensures you get the full “bonus” from your company.

The $1,000 a Month Rule: Setting a Tangible Goal

“How much do I actually need in my 401k to live comfortably?” A popular benchmark is the $240k per $1k Rule.

To generate $1,000 per month in retirement income (using a safe withdrawal rate of roughly 4-5%), you generally need to have approximately $240,000 saved in your nest egg.

The Math:

Want $2,000/month? Aim for $480,000.

Want $4,000/month? Aim for $960,000.

By calculating your paycheck deduction today, you can see if you are on track to hit these specific monthly income targets.

Frequently Asked Questions

While the standard benchmark is 15%, contributing 20% is an excellent way to fast-track your retirement. However, it is only "too much" if it prevents you from paying for essential needs, building an emergency fund, or paying off high-interest debt. Ensure you stay within the 2026 IRS limit of $24,500 ($32,500 if age 50+) to avoid tax penalties.

This is a common point of confusion. 401k contributions are deducted before Federal Income Tax, which is why your tax bill goes down. However, they are deducted after FICA taxes (Social Security and Medicare). You must still pay FICA taxes on your full gross earnings, regardless of how much you put into your 401k.

If you exceed the IRS limit (e.g., contributing more than $24,500 across multiple jobs), you must take action before April 15th of the following year.

You need to request an "excess deferral" distribution from your plan administrator.

If you don't remove the extra money in time, you could be taxed twice on that amount—once in the year you earned it and again when you withdraw it in retirement.

You are not locked into your percentage for the whole year. Most employers allow you to change your contribution rate at any time through your payroll portal or HR dashboard.

To Max Out: If it’s late in the year and you haven't saved much, you can temporarily increase your percentage to "catch up."

To Save Cash: If you have an unexpected expense, you can lower your percentage to 0% for a few months and then increase it again later.

Take Control of Your Future Paycheck

Understanding how to calculate your 401k contribution is about more than just math—it’s about knowing exactly where your hard-earned money is going. By mastering these calculations, you can strategically lower your tax bill today while building a substantial nest egg for tomorrow. Whether you choose a Traditional 401k for immediate tax relief or a Roth for tax-free growth, the most important step is simply to start.

Remember, even small adjustments of 1% or 2% can lead to hundreds of thousands of dollars in difference over a long career. Don’t let the complexity of payroll deductions stop you from maximising your financial potential in 2026.

Ready to see your exact numbers?

Now that you know the formula, let our interactive tool do the heavy lifting for you. Use our 401k Calculator — See How Your Paycheck and Retirement Grow to instantly estimate your future savings and see the real impact on your take-home pay.